%%{init: {

"theme": "neutral",

"fontsize": "12px",

"flowchart": { "curve": "basis" }

}}%%

flowchart TD

classDef bigNode fill:#ffffff,stroke:#333,stroke-width:1.5px,font-size:18px,padding:18px;

classDef smallNode fill:#ffffff,stroke:#333,stroke-width:1.5px,font-size:12px,padding:8px;

classDef noteNode fill:#ffffff,stroke-dasharray:3 3,stroke:#555,font-size:12px;

subgraph Splits[ ]

direction TB

T["TRAIN (~60–70%<br>of data)"]:::bigNode

V["VALIDATION<br>(~15–20%)"]:::smallNode

Te["TEST<br>(~15–20%)"]:::smallNode

end

T -->|train models| V

V -->|tune &<br>try again| T

V -->|final chosen<br> model| Te

Note["[Note] Never tune on TEST"]:::noteNode

Te -.-> Note

M13: Train/validation/test splits & cross-validation

CSCI 3151 — Foundations of Machine Learning

Baseline model & metrics

Code

baseline_clf = Pipeline([

("scaler", StandardScaler()),

("logreg", LogisticRegression(max_iter=1000, random_state=42)),

])

baseline_clf.fit(X_train, y_train)

y_train_pred = baseline_clf.predict(X_train)

y_test_pred = baseline_clf.predict(X_test)

print("Train accuracy: {:.3f}".format(accuracy_score(y_train, y_train_pred)))

print("Test accuracy: {:.3f}".format(accuracy_score(y_test, y_test_pred)))

print("Test recall: {:.3f}".format(recall_score(y_test, y_test_pred)))Train accuracy: 0.959

Test accuracy: 0.960

Test recall: 0.077Code

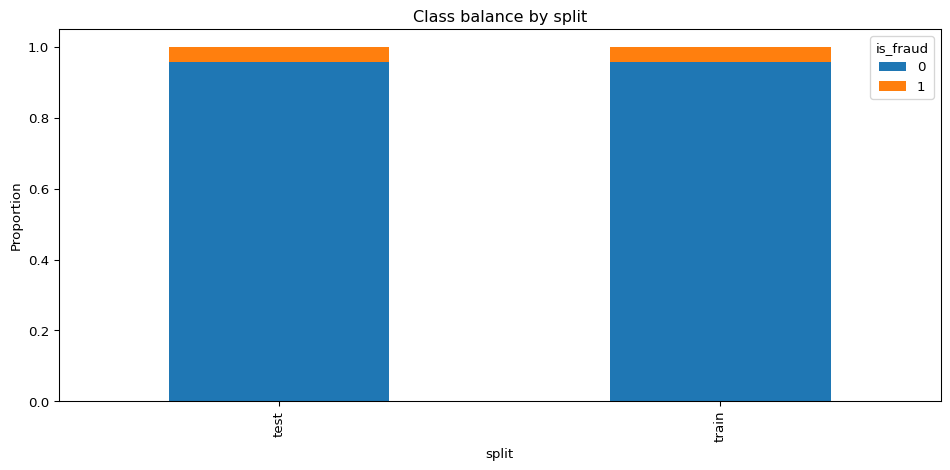

# Plot class balance in train vs test

split_labels = ["train"] * len(y_train) + ["test"] * len(y_test)

y_all = np.concatenate([y_train, y_test])

balance_df = pd.DataFrame({

"split": split_labels,

"is_fraud": y_all,

})

class_counts = (

balance_df

.groupby(["split", "is_fraud"])

.size()

.reset_index(name="count")

)

pivot = class_counts.pivot(index="split", columns="is_fraud", values="count")

pivot = pivot.div(pivot.sum(axis=1), axis=0)

pivot.plot(kind="bar", stacked=True)

plt.ylabel("Proportion")

plt.title("Class balance by split")

plt.legend(title="is_fraud", loc="best")

plt.tight_layout()

plt.show()

- Fraud team cares more about recall on fraud than raw accuracy.

- Our split and metrics must reflect that.

Tuning regularization with \(k\)-fold CV

In LogisticRegression, the hyperparameter C controls how strong the L2 regularization is:

- Smaller

C⟶ stronger regularization

(weights are shrunk more, decision boundary smoother, less overfitting). - Larger

C⟶ weaker regularization

(weights can grow, boundary can be more wiggly, more risk of overfitting).

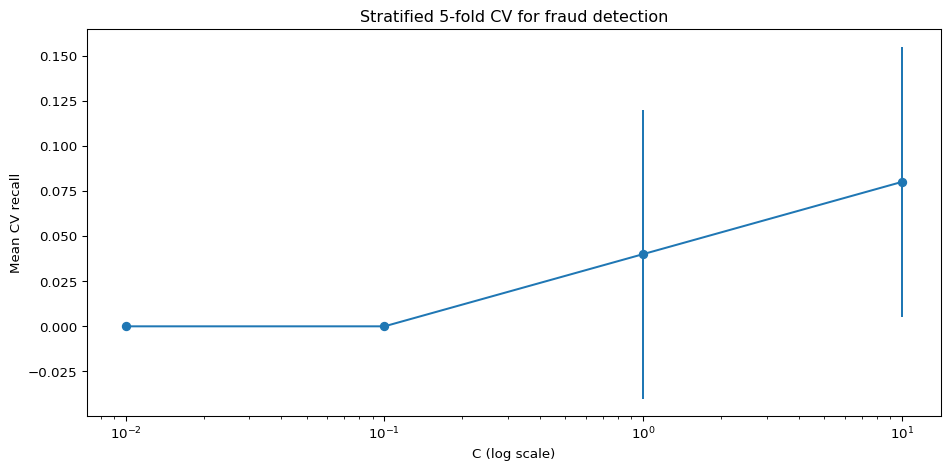

We don’t guess C by eye. Instead, we use \(k\)-fold cross-validation on the training set:

- Pick a grid of candidate values, e.g.

C ∈ {0.01, 0.1, 1, 10, 100}. - For each

C, run \(k\)-fold CV and compute the mean validation score (and optionally its std). - Choose the

Cwith the best mean performance (subject to being reasonably stable).

Code

# First: split off a test set

X_train_val, X_test, y_train_val, y_test = train_test_split(

X,

y,

test_size=0.2,

stratify=y,

random_state=42,

)

def make_model(C):

return Pipeline([

("scaler", StandardScaler()),

("logreg", LogisticRegression(C=C, max_iter=1000, random_state=42)),

])

skf = StratifiedKFold(n_splits=5, shuffle=True, random_state=42)

Cs = [0.01, 0.1, 1.0, 10.0]

rows = []

for C in Cs:

model = make_model(C)

scores = cross_val_score(

model,

X_train_val,

y_train_val,

cv=skf,

scoring="recall", # emphasize catching fraud

n_jobs=None,

)

rows.append({"C": C, "mean_recall": scores.mean(), "std_recall": scores.std()})

cv_df = pd.DataFrame(rows).sort_values("C")

cv_df| C | mean_recall | std_recall | |

|---|---|---|---|

| 0 | 0.01 | 0.00 | 0.000000 |

| 1 | 0.10 | 0.00 | 0.000000 |

| 2 | 1.00 | 0.04 | 0.080000 |

| 3 | 10.00 | 0.08 | 0.074833 |

Code

Code

np.float64(10.0)Code

precision recall f1-score support

0 0.963 1.000 0.981 287

1 1.000 0.154 0.267 13

accuracy 0.963 300

macro avg 0.982 0.577 0.624 300

weighted avg 0.965 0.963 0.950 300