M16 - Scaling, encoding, binning, feature creation

CSCI 1109 — Practical Data Science

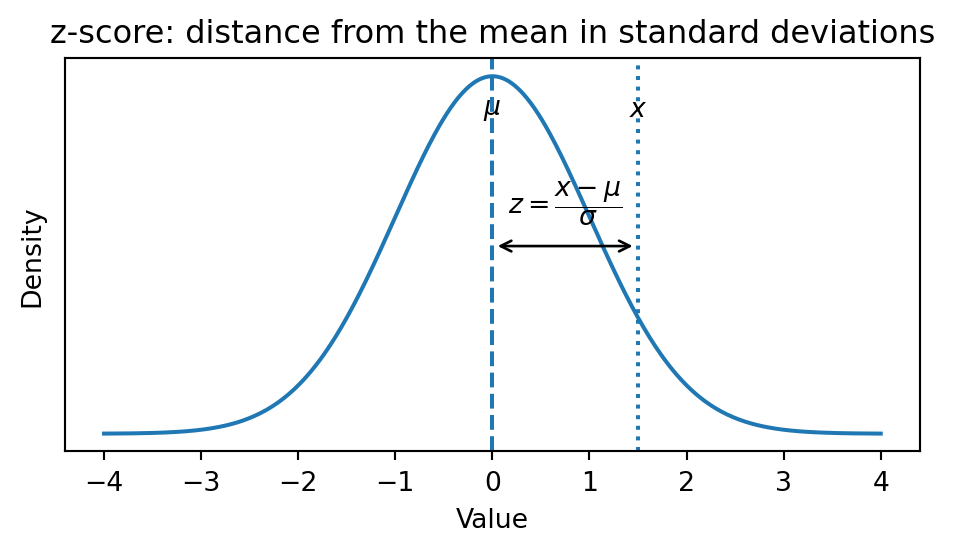

Scaling: standardization (z-scores)

Intuition:

Measure “how many standard deviations away from typical” a value is.

Formal definition for a feature \(x\):

- Mean: \(\mu = \frac{1}{n} \sum_{i=1}^n x_i\)

- Standard deviation: \(\sigma = \sqrt{\frac{1}{n} \sum_{i=1}^n (x_i - \mu)^2}\)

- 👉 Standardized value: \[ z_i = \frac{x_i - \mu}{\sigma} \]

Tiny numeric example (monthly income in $1,000s):

| person | raw income | standardized \(z\) (approx) |

|---|---|---|

| A | 2.0 | -0.7 |

| B | 3.0 | 0.0 |

| C | 4.0 | 0.7 |

🔎 Interpretation: B is “typical”, A is 0.7 standard deviations below typical, C is 0.7 above.

Note

Scaling your data with the z-score is like fitting a Normal curve to your data, then (1) moving it to have 0 mean and (2) stretching it to have standard deviation of 1.

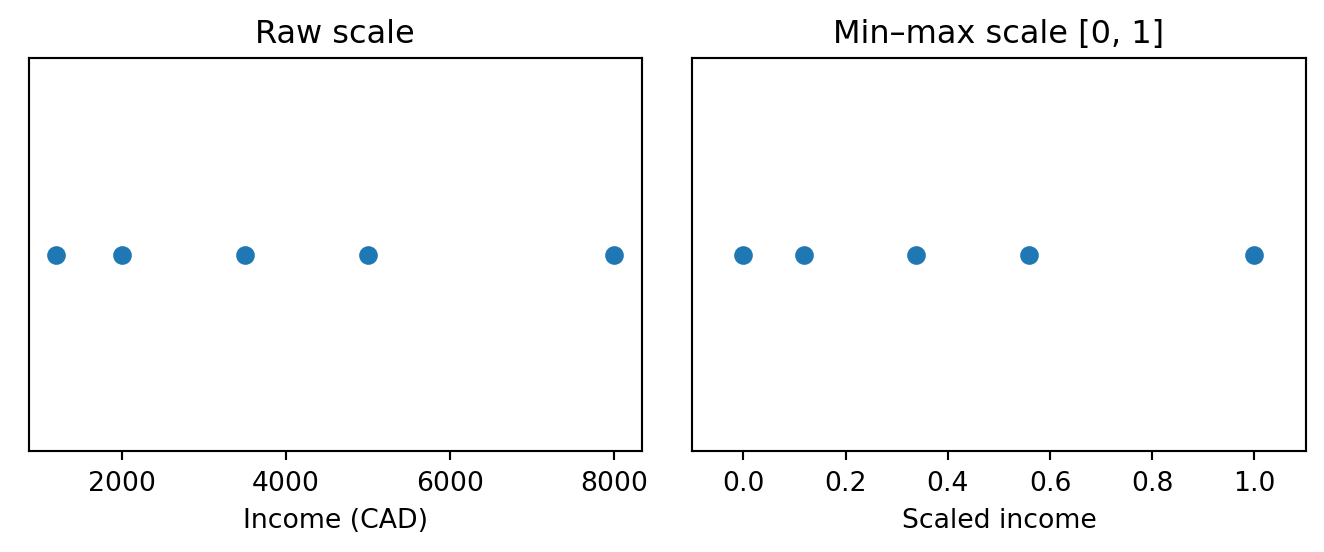

Scaling: min–max (0–1) scaling

Intuition:

Stretch or compress feature values so the minimum becomes 0 and the maximum becomes 1.

Formula for feature \(x\):

\[ x_i^{(scaled)} = \frac{x_i - x_{\min}}{x_{\max} - x_{\min}} \]

Use cases:

- For algorithms that assume all features are in similar numeric ranges (e.g., distance-based).

- For visualizations where you want features to be directly comparable.

Risk: outliers can make the min–max range huge; consider clipping or robust variants.

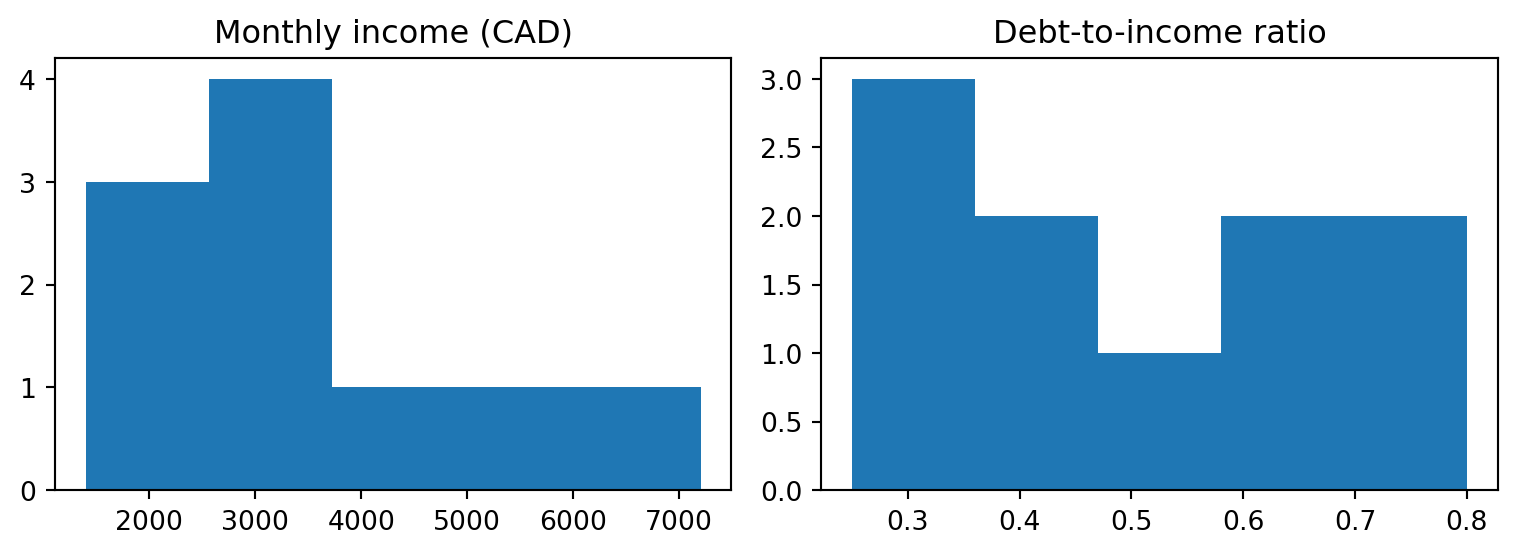

Inspect raw scales

| loan_id | age | monthly_income | debt_to_income | defaulted | |

|---|---|---|---|---|---|

| count | 10.00000 | 10.000000 | 10.000000 | 10.000000 | 10.000000 |

| mean | 5.50000 | 38.100000 | 3390.000000 | 0.505000 | 0.400000 |

| std | 3.02765 | 11.445038 | 1725.913607 | 0.183258 | 0.516398 |

| min | 1.00000 | 22.000000 | 1400.000000 | 0.250000 | 0.000000 |

| 25% | 3.25000 | 30.000000 | 2225.000000 | 0.362500 | 0.000000 |

| 50% | 5.50000 | 37.000000 | 3000.000000 | 0.500000 | 0.000000 |

| 75% | 7.75000 | 44.000000 | 3950.000000 | 0.637500 | 1.000000 |

| max | 10.00000 | 60.000000 | 7200.000000 | 0.800000 | 1.000000 |

Things to notice:monthly_incomeis in thousands of dollars;debt_to_incomeis 0–1.- A 1-unit change in

monthly_incomevsdebt_to_incomedoes not mean the same thing. - Distance-based methods would mostly “see” differences in income, not debt ratio.

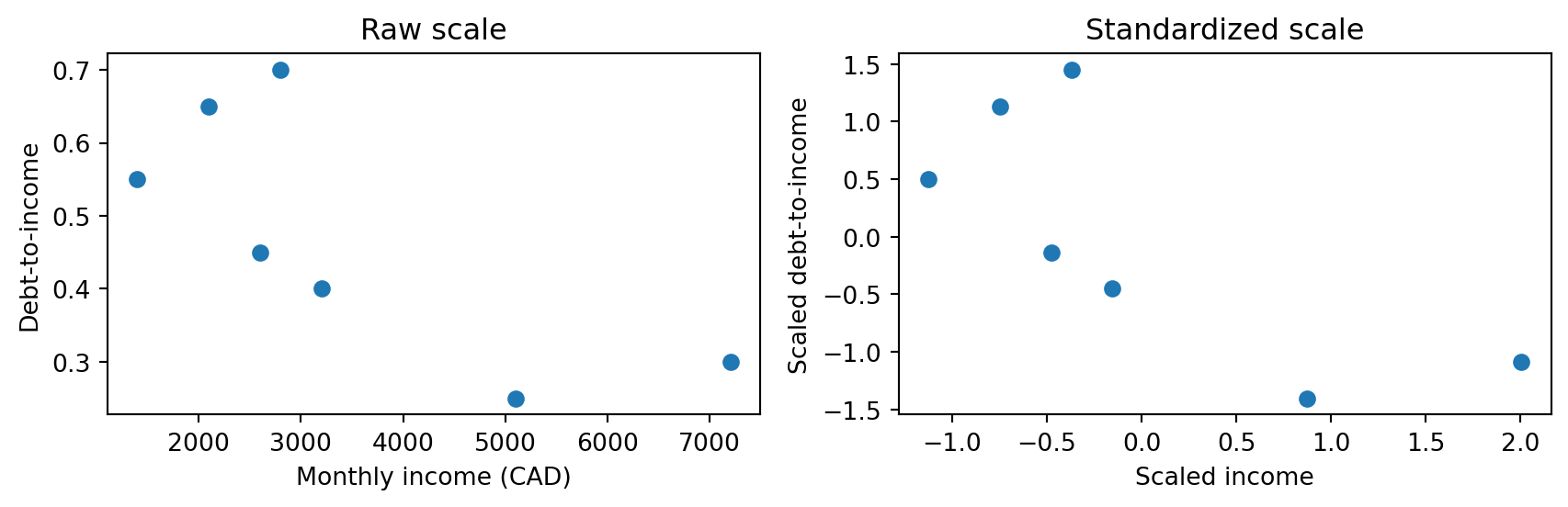

Let’s visualize:

Visualizing before vs after scaling

Code

fig, axes = plt.subplots(1, 2, figsize=(9, 3))

axes[0].scatter(train["monthly_income"], train["debt_to_income"])

axes[0].set_xlabel("Monthly income (CAD)")

axes[0].set_ylabel("Debt-to-income")

axes[0].set_title("Raw scale")

axes[1].scatter(train_scaled["monthly_income"], train_scaled["debt_to_income"])

axes[1].set_xlabel("Scaled income")

axes[1].set_ylabel("Scaled debt-to-income")

axes[1].set_title("Standardized scale")

plt.tight_layout()

Interpretation:

- On the left, income dominates the horizontal scale.

- On the right, both axes are roughly [-2, 2], so distance-based algorithms would treat income and debt_ratio more symmetrically.

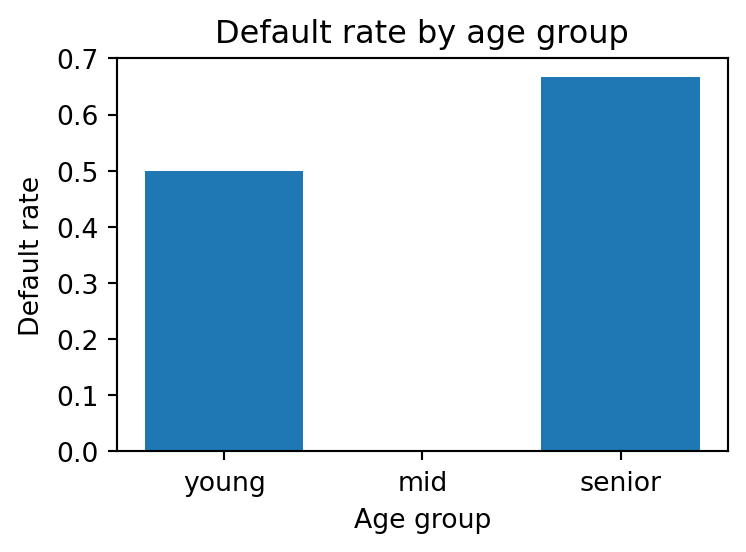

Binning age and inspecting default rate

We’ll bin age into groups and look at default rates.

Code

| age | age_group | defaulted | |

|---|---|---|---|

| 0 | 22 | young | 0 |

| 1 | 35 | mid | 0 |

| 2 | 41 | mid | 0 |

| 3 | 29 | young | 1 |

| 4 | 60 | senior | 1 |

| 5 | 50 | senior | 0 |

| 6 | 33 | mid | 0 |

| 7 | 45 | senior | 1 |

Now compute default rate by age group:

Code

| age_group | default_rate | |

|---|---|---|

| 0 | young | 0.500000 |

| 1 | mid | 0.000000 |

| 2 | senior | 0.666667 |

Plot it:

Code

🤔 Interpretation:

- Even with tiny data, we can see whether certain age ranges appear riskier.

- In real data, we’d need more rows and proper uncertainty quantification before acting.